There’s a growing threat in pharmaceutical patient access that most manufacturers know exists, but far too few are actually measuring or combating.

Alternative Funding Programs – AFPs – have become the villain of choice in GTN conversations. And for good reason. They’re real, they’re disruptive, and they’re growing. But in our work running real-time PAP analysis across major drug brands, we’re seeing something that deserves equal attention: the patients quietly draining your PAP aren’t just AFP enrollees. Many of them – and sometimes most of them – are maximizer and accumulator patients, and they’ve been there all along.

If you work in market access, patient services, or GTN strategy, this one is worth your full attention.

1. AFPs Do More Than Just Create Leakage – They Break the Patient Experience

Let’s start with AFPs, because understanding how they work matters for everything that follows.

An alternative funding vendor advises a health plan to remove a specific high-cost drug from the covered drug list and reclassify it as a “non-essential health benefit.” Overnight, a patient who had active commercial insurance is now effectively uninsured for their medication. They’re ineligible for your copay program. They can’t afford the drug at retail. So the AFP steps in and enrolls them into your Patient Assistance Program (PAP) instead.

The result? Your charitable program – designed for patients who are truly uninsured or underinsured – is now subsidizing patients who do have coverage, coverage that was removed on purpose. Meanwhile, that patient has lost continuity of care, lost access to their copay support, and in many cases has no idea why.

This isn’t an edge case. It’s a growing, deliberate strategy. But it’s also, it turns out, not the whole story.

2. Your PAP Is More Exposed Than You Think – And It’s Not Just AFPs

Most manufacturers have eligibility criteria designed to screen out commercially insured patients from their PAPs. The problem is that AFPs, maximizers, and accumulators are all engineered – in different ways – to make insured patients look eligible for programs they shouldn’t be in. Standard benefit verification often misses it.

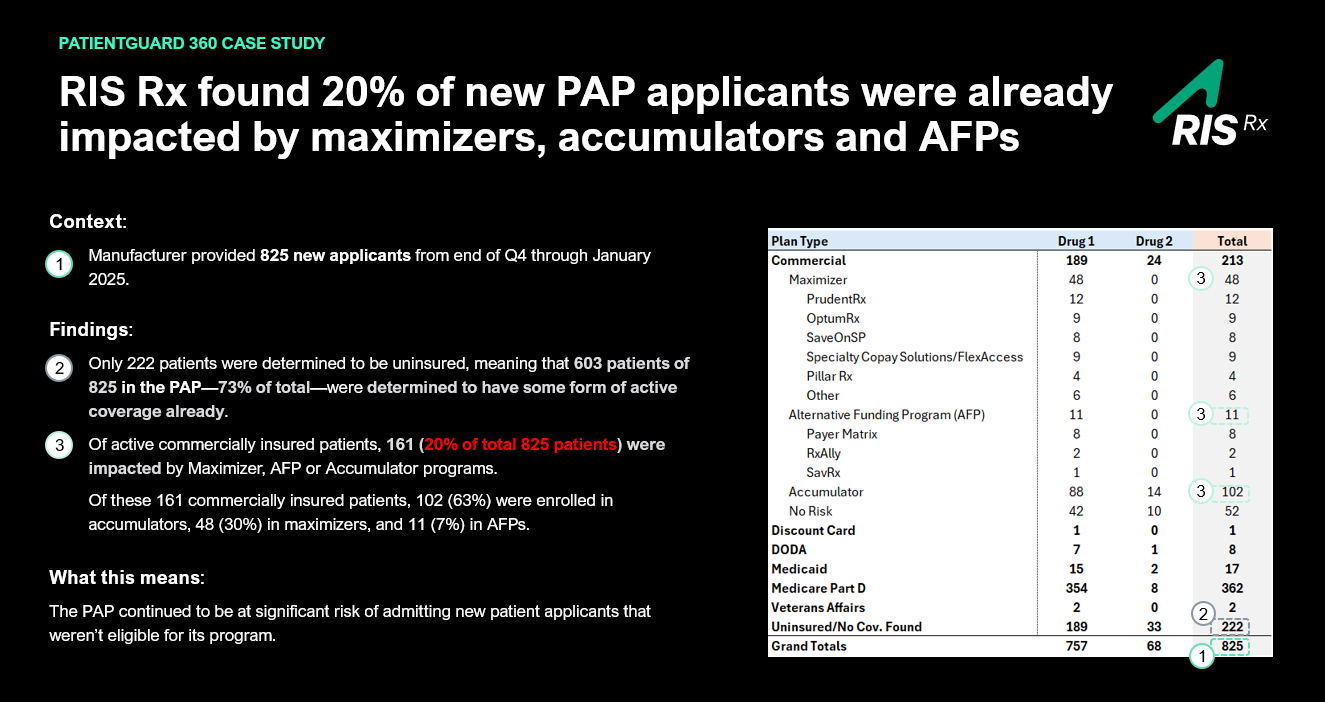

In a pilot study conducted by RIS Rx using our PatientGuard 360 product, we analyzed 825 new PAP applicants submitted by a manufacturer over a defined period at the end of Q4 2024 and into January 2025.

The findings were stark:

- Of 213 patients with active commercial insurance, 161 were impacted by a maximizer, AFP, or accumulator program – that’s 20% of all 825 patients.

- And here’s where it becomes important: the breakdown of those 161 commercially insured patients tells a different story than most people expect:

- Accumulator patients: 102 (63%)

- Maximizer patients: 48 (30%)

- Patients impacted by AFPs: 11 (7%)

In other words: one out of five patients entering that PAP had active, robust commercial coverage already. Of those commercially insured patients, the overwhelming majority weren’t AFP enrollees at all, they were accumulator and maximizer patients.

AFP exposure was real, but it was only a fraction of the problem.

It’s worth noting that not all patients with active coverage are automatically ineligible for PAP. Many programs intentionally include Medicare Part D patients, who often face significant out-of-pocket exposure despite having coverage. The real concern is commercially insured patients being steered into PAPs by accumulators, maximizers, and AFPs that are specifically designed to exploit charitable assistance programs.

3. The AFP Playbook Is Evolving – But So Are the Other Threats

One of the most important things we said on our recent Xtalks webinar is that AFPs are no longer a fringe tactic. They are increasingly targeting chronic disease categories and specialty drugs – precisely the programs with the highest per-patient costs and the most vulnerable patient populations.

But the same is true of maximizers and accumulators. Their designs continue to evolve, regulatory responses remain inconsistent, and they’re appearing across a broader range of therapeutic categories than ever before. What worked to catch any of these programs last year may not work this year.

Leading manufacturers are responding by treating PAP eligibility screening as a dynamic, real-time problem, not a one-time setup exercise. Those who aren’t doing this yet are operating in the dark. The threat isn’t one bad actor. It’s a structural misalignment between how benefit design works in the market and how most PAP eligibility processes were built.

4. The Data Asymmetry Problem Is the Root Cause – and It Works Against You

Why are PAPs so vulnerable to AFPs, maximizers, and accumulators? Because no single stakeholder in the patient access chain sees the full picture.

Manufacturers know what their programs are designed to do. PBMs and payers know what their plan designs say. Specialty pharmacies know what they adjudicate. But the moment any of these programs reclassifies a patient’s insurance status, or quietly manipulates how copay spend is counted, the signal that something is wrong rarely reaches the manufacturer at enrollment. By the time it shows up in a GTN reconciliation report, the damage is done.

This is what we call data asymmetry: the gap between what’s happening in real time and what manufacturers can actually see. PAP exposure to AFPs, maximizers, and accumulators doesn’t announce itself. It gathers quietly, one misrouted patient at a time.

The manufacturers getting ahead of this problem are the ones who have moved from retroactive auditing to real-time, enrollment-first detection, segmenting patients at the moment they apply, before a single dollar flows through the wrong channel.

5. Solving for This Isn’t Just a Revenue Play – It’s a Patient Safety Issue

This point tends to get lost in GTN discussions, and it shouldn’t.

Whether a patient is diverted by an AFP, enrolled inappropriately as a result of a maximizer, or misrouted due to accumulator complexity, the clinical impact is the same: re-enrollment cycles every 3, 6, or 12 months, potential gaps in therapy, and disrupted continuity of care. Patients in specialty categories (i.e. oncology, immunology, neurology) can’t afford those gaps. The stakes are clinical, not just financial.

There’s also a compliance dimension. PAPs have terms and conditions. When patients who don’t qualify are admitted at scale, regardless of the mechanism, it creates documentation risk, eligibility exposure, and operational strain on the teams managing those programs. Getting enrollment right the first time isn’t just about protecting margin. It’s about protecting the program’s integrity and the patients it was built to serve.

What We Built to Solve This

PatientGuard 360 (PG360) is RIS Rx’s PAP-and free-goods-based leakage solution. It identifies patients at point of enrollment, and segments them according to their true benefit status, whether the exposure is an AFP, a maximizer, an accumulator, or another eligibility issue. Commercially insured patients are redirected to appropriate copay support. Ineligible patients are flagged before they consume charitable resources intended for others.

PG360 operates as an extension of your existing operations, not a replacement. It integrates via direct API or secure batch file, delivers cloud-based reporting, and is designed to scale as your program grows and benefit design complexity increases.

The pilot data speaks for itself. If one in five of your new PAP applicants have active commercial coverage, and the majority of those are accumulator and maximizer patients, not AFPs, then the question isn’t whether this problem exists in your program.

The question is whether you’re measuring it. And whether you’re measuring all of it.

If you’d like to see how PAP exposure is affecting your specific program, the RIS Rx team is available for a custom analysis. Reach out to stephen@risrx.com or get in touch with our expert team at risrx.com to learn more.